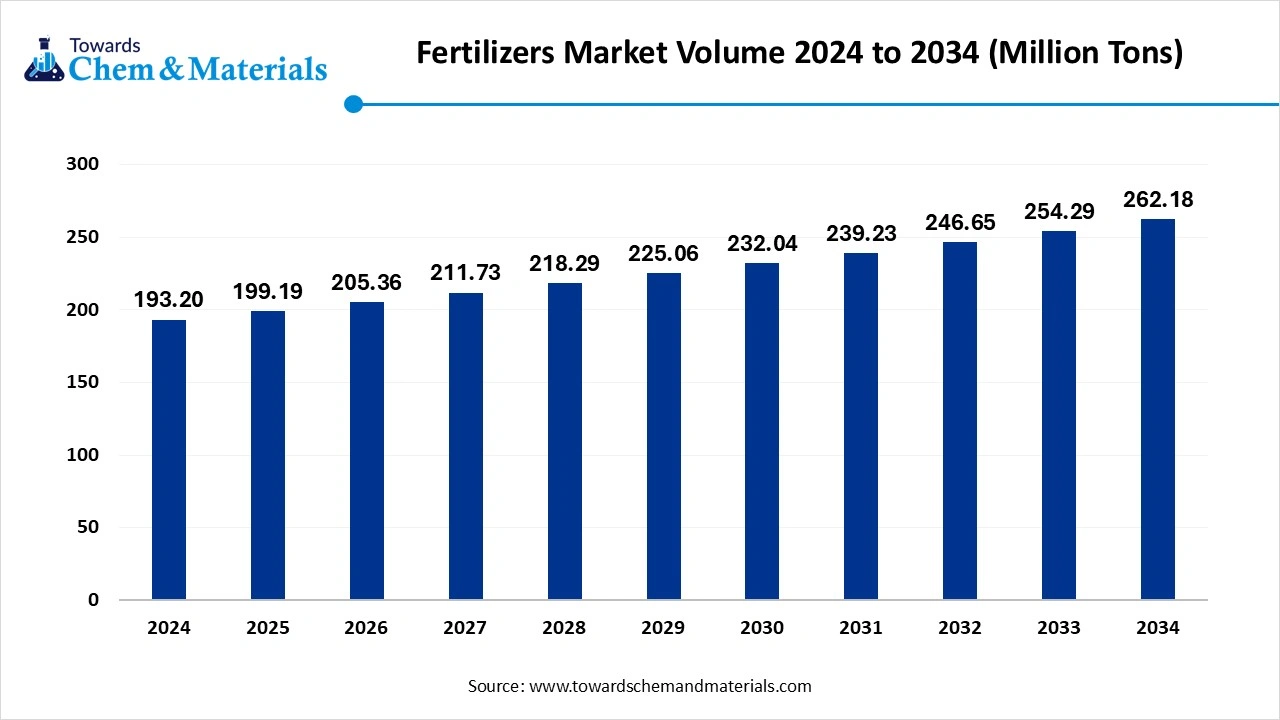

Fertilizers Market to Reach 262.18 Million Tons by 2034 Amid Increasing Demand

According to Towards chem and Materials consultants, the global fertilizers market volume reached 199.19 million tons in 2025 and is forecast to witness steady growth, touching nearly 262.18 million tons by 2034 at a CAGR of 3.10% from 2025 to 2034. Asia Pacific dominated the Asia Pacific fertilizers market with Volume Share of 52.08% in 2024.

Ottawa, July 09, 2025 (GLOBE NEWSWIRE) -- According to Towards chem and Materials consultants, the global fertilizers market volume reached 193.20 million tons in 2024 and is projected to hit around 262.18 million tons by 2034.a study published by Towards chem and Materials a sister firm of Precedence Research.

Get All the Details in Our Solutions –Download Sample: https://www.towardschemandmaterials.com/download-sample/5578

The market is driven by concerns regarding food security, decreasing cultivable land, and increased demand for food crops. Technological advances and favourable national and international agricultural policies also fuel its strategic growth.

Fertilizers are essential agricultural inputs that can improve soil fertility and crop productivity through the application of key macronutrients such as nitrogen, phosphorus, and potassium. In today's world, fertilizers have become a critical input, specifically due to rising food demand globally and significantly less arable land per capita. In the fields of agriculture, particularly in Asian and African regions, a growing trend towards intense farming is leading to increased fertilizer usage.

Currently, the fertilizers market is undergoing transformation through innovation in eco-friendly and precision fertilizers to improve productivity sustainably. Increased regulation and damage done to the environment from nutrient runoff have further increased producer spending on slow-release and bio-fertilizers. At the same time, digital agriculture and smart farming applications are now promoting the efficient usage of fertilizers while placing more emphasis on productivity while also minimizing environmental risks.

Key Takeaways

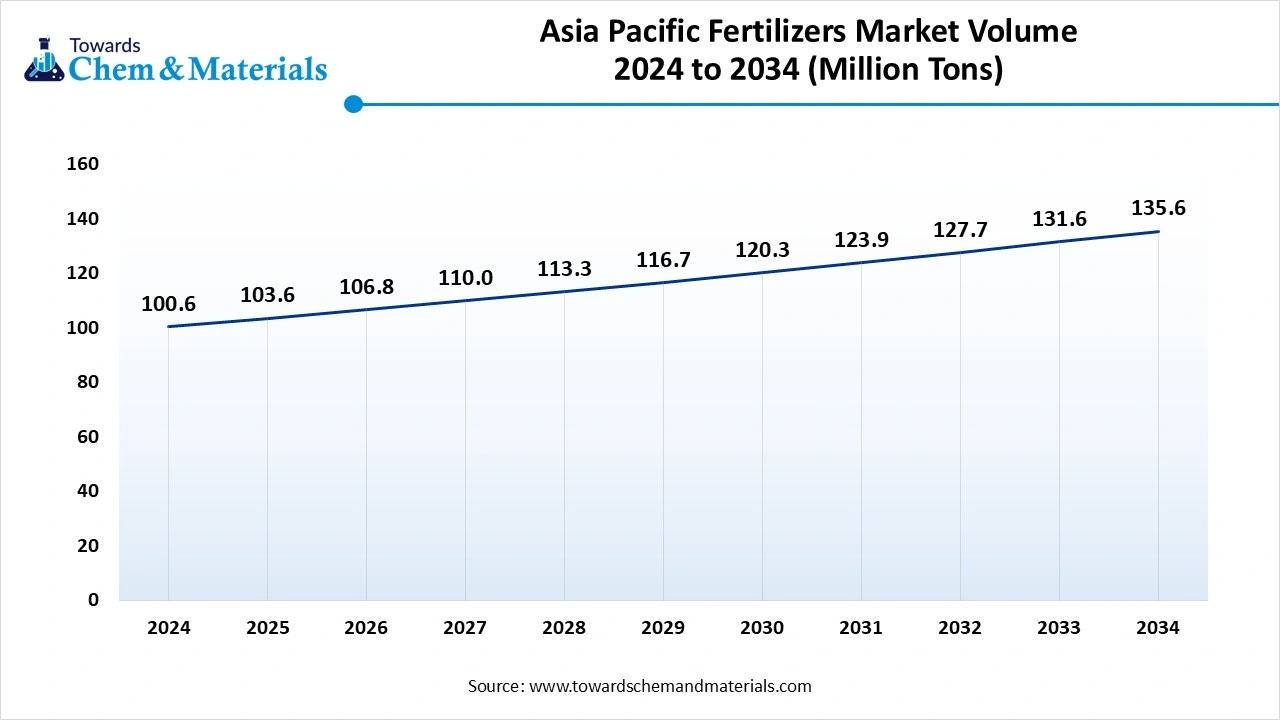

- The Asia Pacific fertilizers market Volume was valued at 100.6 million tons in 2024 and is expected to be worth around 135.56 million tons by 2034, growing at a compound annual growth rate (CAGR) of 3.02% over the forecast period 2025 to 2034.

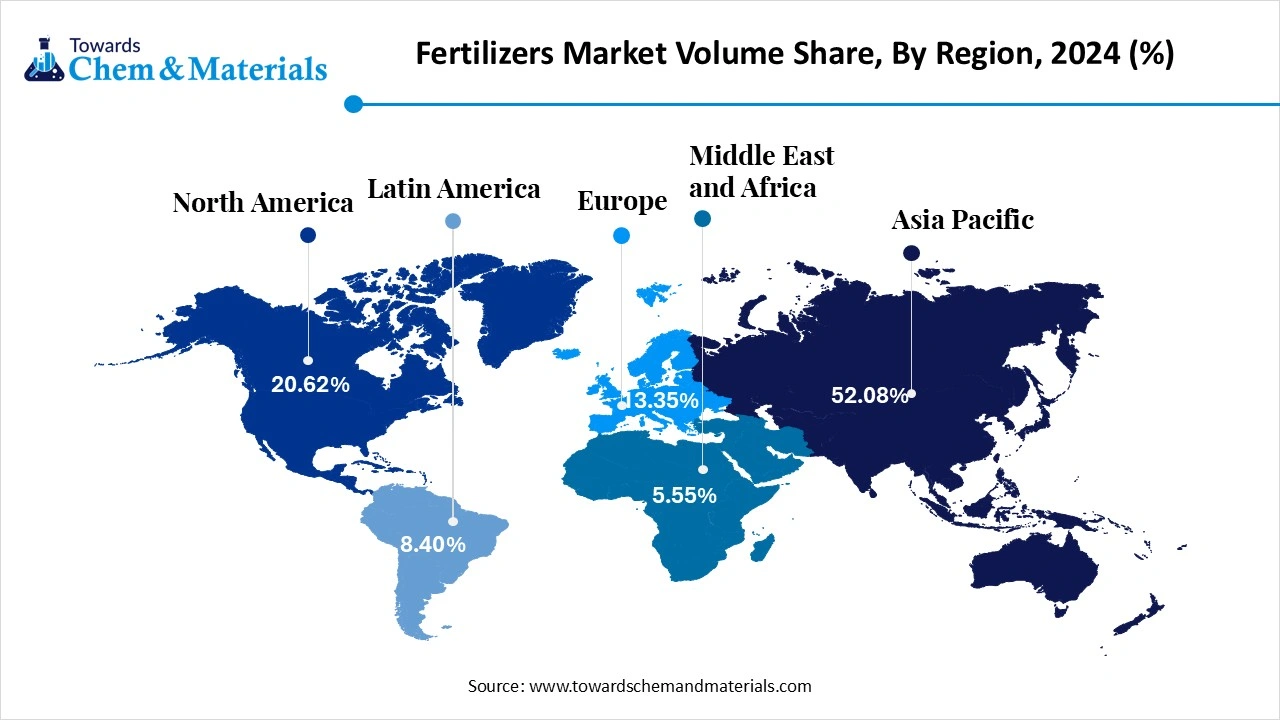

- The Asia Pacific fertilizers dominated the global market and accounted for the largest Volume Share of 52.08% in 2024.

- The North America fertilizers market is expected to grow at a CAGR of 2.76% over the forecast period.

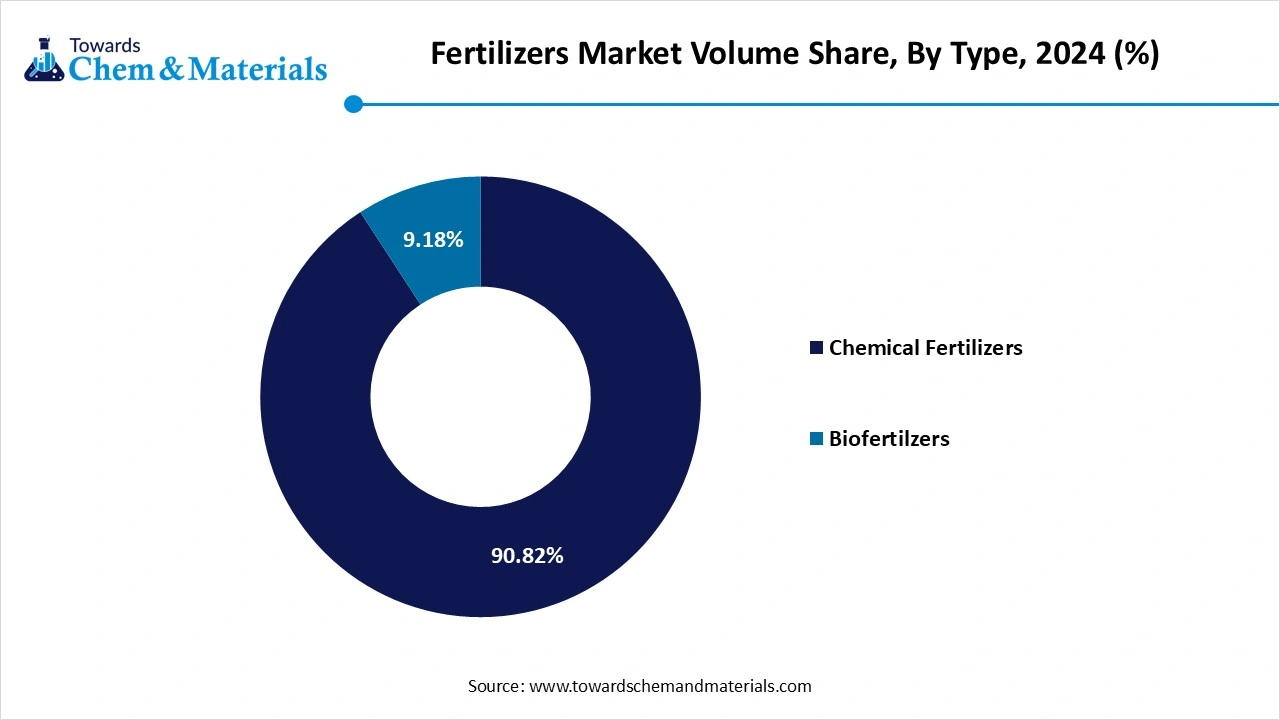

- By type, the chemical fertilizers segment led the market and accounted for the largest Volume Share of 90.82% in 2024

- By type, the biofertilizers segment is expected to grow at a CAGR of 4.47% over the forecast period.

- By form, the solid fertilizers segment led the market with the largest Volume Share of 84.3% in 2024.

- By form, the liquid fertilizers segment is expected to grow at a CAGR of 3.93 over the forecast period

- By crop type, the Cereals & Grains segment led the market with the largest Volume Share of 42.76% in 2024.

- By crop type, the fruits & vegetables segment is expected to grow at a CAGR of 3.05% over the forecast period

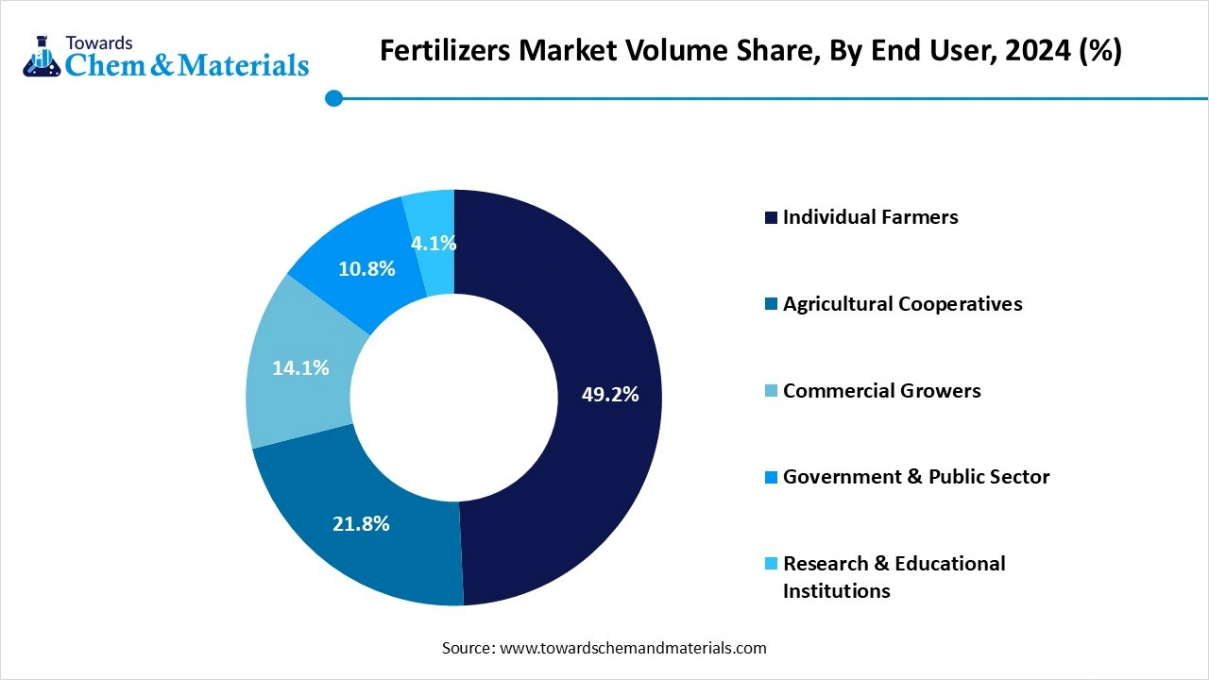

- By end-user, the individual farmers segment led the market and accounted for the largest Volume Share of 49.2% in 2024

- By end-user, the commercial grower’s segment is expected to grow at a CAGR of 3.72% over the forecast period.

- By distribution channel, the distributors & wholesalers segment led the market with the largest Volume Share of 41.1% in 2024.

- By distribution channel, the Online/E-commerce platforms segment is expected to grow at a CAGR of 3.49% over the forecast period.

Explore Strategic Figures & Forecasts – Access the Databook | Immediate Delivery Available: https://www.towardschemandmaterials.com/download-databook/5578

Fertilizers Market Report Scope

| Report Attribute | Details |

| Market Volume in 2025 | 199.19 Million Tons |

| Expected Volume by 2034 | 262.18 Million Tons |

| Growth rate | CAGR of 3.10% from 2025 to 2034 |

| Base year for estimation | 2024 |

| Historical data | 2020 - 2024 |

| Forecast period | 2025 - 2034 |

| Quantitative Units | Volume in kilotons, revenue in USD million, and CAGR from 2025 to 2034 |

| Report coverage | Revenue forecast, competitive landscape, growth factors, and trends |

| Segments covered | By Form, By Type, By Crop Type, By Application, By End User, By Distribution, By Region |

| Key companies profiled | Nutrien Ltd, Yara, ICL,The Mosaic Company, CF Industries and Holdings, Inc., Nufarm, SQM SA, OCP Group, K+S Aktiengesellschaft, Eurochem Group, Sociedad Quimica y Minera de Chile SA |

Invest in Premium Global Insights Immediate Delivery Available @ https://www.towardschemandmaterials.com/price/5578

What are the Major Trends in the Fertilizers Market?

Increase in the Demand for Bio-based and Organic Fertilizers

Increasing environmental concerns and chemical-use regulations are pushing farmers in the direction of organic and bio-based fertilizers. These products improve soil fertility, have a lesser impact on the environment, and align with the growing consumer desire for sustainability in food production and farming systems, particularly in developed markets and among organic food producers.

Advancements in Precision Agriculture

Innovation in the use of precision agriculture tools (GPS mapping, drones, and smart sensors) are improving the way fertilizer is applied. These technologies allow farmers to apply nutrients in the right proportion, on the right crop, and at the right time, resulting in improved efficiency, lower costs, and reduced environmental impacts by using more targeted means of fertilization.

Growth of Specialty Fertilizers

Specialty fertilizers like controlled-release, water-soluble, and micronutrient-rich fertilizers are also growing in popularity. These fertilizers are conducive to specific crop needs and region-specific nutritional needs - resulting in improved yield and quality. Farmers are increasingly using specialty fertilizers for high-value crops or in areas with marginal soils or limited water.

Growth Factors in the Fertilizers Market

- Rising Global Food Demand: Population growth and dietary changes are increasing demands for more agricultural production. Fertilizers allow farmers to enable productivity, and to ensure food security, so are being more frequently relied upon in the marketplace.

- Reducing Arable Land- With the growth of cities, and other factors like contamination and degradation reducing the amount of farmland outside of urban areas, farmers are increasingly dependent on fertilizers to maximize production per hectare and maintain consistent quality of crop within a yield.

- Government Assistance & Subsidy- Across the globe, many countries provide subsidies, tax breaks and other incentives to use fertilizers. In many developing regions fertilizer is more affordable and leads to greater uptake.

- Improved Fertilizer Technology- Categories of fertilizer like slow-release, water-soluble fertilizer and bio-based fertilizer are promoting better nutrient availability with less environmental impact and gaining traction in the marketplace including by environmentally conscious farmers and agribusinesses.

How Artificial Intelligence Redefines the Future of Fertilizers?

Fertilizer management is increasingly relying on artificial intelligence (AI) to facilitate data-informed and site-specific fertilizer application. The most recent applications of AI have reduced nitrogen waste by up to 25% with similar yields. Using advanced algorithms, models accounted for soil health, crop type and planned harvest, and meteorological conditions, and then predicted the most effective volumetric dosages. The AI process then generates accurate recommendations, reducing nutrient runoff in the environment and concurrently improving consistency in yield in the farm.

Maharashtra's ₹500 crore "MahaAgri-AI Policy 2025-29" showcases the growing institutional support for this AI machinery and mission. This policy includes support for sensors, drones, and advisory systems in the intended fertilizer use. Meanwhile, global agritech companies are utilizing AI incorporated with satellite imagery and IoT data to automate real-time fertilizer recommendations. This is not only economic efficiency, but reduces environmental risk, improves returns on inputs, and is much closer to carbon reduction targets.

Could Global Shift Towards Green Fertilizers Presents Big Market Opportunity?

The shift to green fertilizer is a strong growth opportunity, which is being accelerated by both rising climate concerns and government-led initiatives. Traditional nitrogen-based fertilizers account for almost 5% of global GHG emissions, and green alternatives, such as fertilizers produced through renewable powered ammonia can achieve a total reduction of GHG by as much as 90%. As an example, Yara just recently partnered with PepsiCo to supply low-carbon fertilizers to 1,000 farms in Europe by 2025. Also, Fertiglobe’s recent deal to sell green ammonia for €1,000/ton under the EU's H2Global scheme, this is further proof that there is demand in the marketplace for green fertilizers.

There are also large-scale developments of green ammonia plants getting off the ground in both Paraguay and Brazil, showing that the momentum is truly global. Green fertilizers are now a pillar of agriculture's future, especially as the shift from harmful conventional fertilizers is increasingly supported through climate policies and sustainability objectives.

Limitations and Challenges in the Fertilizers Market

- Environmental and Regulatory Challenges- Restrictive environmental regulations related to fertilizer use are limiting fertilizer input in farming as a reaction to soil degradation, water pollution, and greenhouse gas emissions. A growing global effort to push for a sustainable agricultural sector restricts further expansion of chemical fertilizers.

- Uncertainty in Raw Material Prices- The traditional fertilizer production process uses a large input of natural gas, phosphate, and potash. Depending on changes in prices or geopolitical concerns impacting supply networks, it can increase the production cost, and in turn, reduce profitability for manufacturers and affordability to farmers.

-

Soil Health Issues and Dependency- Fertilizers harm soil structure and impact microbial diversity, resulting in decreasing fertility over time as a result of excessive mineral fertilizer use. The overdependence on fertilizers will necessitate an adaptation to organic alternatives leading to a decreased demand in organic fertilizer in some provinces.

Fertilizers Market Segmentation

Type Insights

Chemical fertilizers Segment Dominated the fertilizers Market in 2024?

Chemical fertilizers segment dominated the fertilizers market in 2024. The most widely used type reinforces this market still because of the role chemical fertilizers bring to crop production and productivity. Chemical fertilizers provide complete and defined nutrient formulation, which allows growers precision use of plant nutrition. These fertilizers will always support high yield agriculture.

Biofertilizers segment expects the fastest growth in the market during the forecast period, because of environmental and societal issues, however biofertilizers are starting to be adopted and usage is increasing rapidly because of environmental issues and the increasing concern with the efficiency of chemical fertilizers.

Fertilizers Market Volume and Share, By Type, 2024- 2034 (%)

| By Type | Market Volume Shares (%)2024 | Market Volume (Million Tons)2024 | Market Volume Shares (%)2034 | Market Volume (Million Tons)(2034) | Market CAGR (2025-2034) | |||

| Chemical Fertilizers | 90.82 | % | 175.5 | 89.52 | % | 234.7 | 2.95 | % |

| Biofertilizers | 9.18 | % | 17.7 | 10.48 | % | 27.5 | 4.47 | % |

Form Insights

What made Solid Fertilizers the Dominant Segment in the Fertilizers Market in 2024?

The solid fertilizers segment dominated the fertilizers market in 2024. Granular fertilizers are widely accepted and of constant appearance for fertilizers due to ease of use and extended shelf life. Granular fertilizers are favoured by lots of visible farmers when we consider broad-acre farming, predominantly for consistent nutrient composition leading to improved spreadability in developed irrigation regions, allowing for improved nutrient balanced soil and eventual yields.

The liquid fertilizers segment expects the fastest CAGR during the forecast period, due to their rapid absorption rates and ability to be applied to precision farming technologies. Liquid fertilizers are generally soluble in water, so they can be used as fertigation to further increase the delivery efficiency of nutrients. Liquid solutions are overtaking granule or solid products due to horticulture considerations; there is also greater acceptance of controlled irrigation systems in some regions. The greater acceptance of controlled irrigation systems is increasing due to modern technologies like drip watering; this is clearly enhancing the fertilizer solution market in water-constraint regions.

Fertilizers Market Volume and Share, By Form, 2024- 2034 (%)

| By Form | Market Volume Shares (%)2024 | Market Volume (Million Tons) 2024 | Market Volume Shares (%)2034 | Market Volume (Million Tons)(2034) | Market CAGR (2025-2034) | |||

| Solid Fertilizers | 84.3 | % | 162.9 | 83.2 | % | 218.1 | 2.96 | % |

| Liquid Fertilizers | 14.2 | % | 27.5 | 15.4 | % | 40.5 | 3.93 | % |

| Gaseous Fertilizers | 1.5 | % | 2.8 | 1.4 | % | 3.6 | 2.37 | % |

Crop-Type Insights

Why did the Cereals & Grains Segment Dominate the Fertilizers Market in 2024?

Cereals & Grains segment dominated the market in 2024. Cereals & Grains are staple crops such as rice, wheat, and maize which are grown around the world on a large scale, and require a large amount of fertilizer to maintain yield. The need for these staples crops in global food security drives ongoing usage of chemical fertilizer for these crops especially in the Asia-Pacific and North American regions. Increased government support and strong infrastructure further promote adoption.

Fruits & Vegetables segment expects the fastest growth in the market during the forecast period. Increased health consciousness and the demand for high-value products has led to this rapid growth. These crops require a precise application of nutrients, and require high-value advanced fertilizers such as foliar sprays and fertigation applications.

Fertilizers Market Volume and Share, Crop Types, 2024 (%)

| By Crop Type | Market Volume Shares (%)2024 | Market Volume (Million Tons)2024 | Market Volume Shares (%)2034 | Market Volume (Million Tons)(2034) | Market CAGR (2025-2034) | |||

| Cereals & Grains | 42.76 | % | 82.6 | 42.30 | % | 110.9 | 2.99 | % |

| Oilseeds & Pulses | 21.25 | % | 41.1 | 21.05 | % | 55.2 | 3.00 | % |

| Fruits & Vegetables | 19.42 | % | 37.5 | 19.32 | % | 50.7 | 3.05 | % |

| Other Crop Types | 16.57 | % | 32.0 | 17.33 | % | 45.4 | 3.56 | % |

By Mode of Application Insights

Which Application Segment Dominates the Fertilizers Market?

Soil segments dominate the market in 2024. Soil provides fertilizers directly through an irrigation system, which comes as a benefit for the crops because they can absorb nutrients immediately, yielding less waste in the fertilizing process. Fertigation is largely used and implemented in commercial or greenhouse farming where precision and optimization of resources are crucial for crop development. It allows the plants to grow to their maximum potential, and is important for high-yield crops in constrained (water) environments.

Fertilizers Market Volume and Share, By Mode of Application, 2024 (%)

| By Mode of Application | Market Volume Shares (%)2024 | Market Volume (Million Tons)2024 | Market Volume Shares (%)2034 | Market Volume (Million Tons)2034 | Market CAGR (2025-2034) | |||

| Foilar Treatment | 11.08 | % | 21.4 | 10.62 | % | 27.8 | 2.66 | % |

| Soil Treatment | 60.28 | % | 116.5 | 60.08 | % | 157.5 | 3.07 | % |

| Seed Treatment | 24.31 | % | 47.0 | 24.21 | % | 63.5 | 3.06 | % |

| Others Mode of Transport | 4.33 | % | 8.4 | 5.09 | % | 13.3 | 4.77 | % |

Foliar segment expects the significant growth in the market during the forecast period. In foliar application, the fertilizer is sprayed directly onto the leaves of the plant so the plant can absorb the nutrients quickly. The foliar application has become increasingly popular in horticulture and high-value crop production as a tool to mitigate crop development with an immediate nutrient deficiency or improve and sustain plant development through sensitive crop/plant development situations.

End User Insights

Why Individual Farmer Segment Dominates the Fertilizers Market in 2024?

Individual Farmers segment holds the largest volume market share in 2024. Individual farmers represent the largest share of fertilizer end-users due to their being the largest part of the four billion farmers in global agriculture. Fertilizer helps farmers to achieve higher crop yields and maintain productivity on their farms. Government subsidies and availability through a local distributor help promote the individual farmer segment, especially in developing countries, where most farms are small-scale.

Commercial Growers segment expects the significant growth in the market during the forecast period. Commercial growers are greatly increasing their fertilizer usage as they implement modern farming practices. The focus on high-value crops, export markets, and use of precision agriculture equipment creates demands for specialized and efficient fertilizers.

Fertilizers Market Volume and Share, By End User, 2024 - 2034(%)

| By End User | Market Volume Shares (%)2024 | Market Volume (Million Tons)(2024) | Market Volume Shares (%)2034 | Market Volume (Million Tons)(2034) | Market CAGR (2025-2034) | |||

| Individual Farmers | 49.2 | % | 95.1 | 48.3 | % | 126.5 | 2.89 | % |

| Agricultural Cooperatives | 21.8 | % | 42.1 | 21.7 | % | 56.9 | 3.04 | % |

| Commercial Growers | 14.1 | % | 27.3 | 15.0 | % | 39.3 | 3.72 | % |

| Government & Public Sector | 10.8 | % | 20.8 | 11.2 | % | 29.3 | 3.48 | % |

| Research & Educational Institutions | 4.1 | % | 7.9 | 3.9 | % | 10.3 | 2.69 | % |

Distribution Channel Insights

Why Distributors & Wholesalers Segment Dominates the Fertilizers Market in 2024?

The distributors & wholesalers segment led the market with the largest market share in 2024, with their expansive supply chains, bulk-buying capabilities, and relationships with manufacturers and farmers. Their ability to guarantee product availability regionally and provide custom service renders them indispensable in conventional agriculture supply chains.

The Online/E-commerce platforms segment is expected to grow at a CAGR over the forecast period, due to increasing access to the internet and smartphones in rural areas, as well as enhanced digital literacy. Farmers prefer convenience, product comparison, home delivery, and expert advice via an online portal. Government intervention and support for digital agriculture continues to drive growth in this area.

Fertilizers Market Volume and Share, By Distribution Channel , 2024 (%)

| By Distribution Channel | Volume (Million Tons)(2024) | Market Shares (%)2024 | Market Volume (Million Tons)(2034) | Market Volume Shares (%) 2034 | Market CAGR (2025-2034) | |||

| Direct Sales | 32.9 | 17.1 | % | 42.1 | 16.1 | % | 2.48 | % |

| Distributors & Wholesalers | 79.4 | 41.1 | % | 107.4 | 41.0 | % | 3.07 | % |

| Retail Stores | 45.7 | 23.7 | % | 64.3 | 24.5 | % | 3.47 | % |

| Online/E-commerce Platforms | 20.2 | 10.4 | % | 28.4 | 10.8 | % | 3.49 | % |

| Cooperatives | 15.0 | 7.8 | % | 20.0 | 7.6 | % | 2.89 | % |

How Did Asia Pacific Dominate the Fertilizers Market in 2024?

The Asia Pacific fertilizers market volume amounted to nearly 103.6 million tons worldwide in 2025 and is expected to rise to around 135.56 million tons by 2034, growing at a healthy CAGR of 3.02% between 2025 - 2034.

Asia Pacific dominated the market in 2024 due to its enormous agriculture base, a growing population and prominence of government support and subsidies for food security. The numerous countries in the Asia Pacific region, particularly those in South and South East Asia, are focused on improving productivity and yields of agricultural products, such as rice, wheat, and pulses. The increasing demand on food production, rising awareness of more advanced agricultural practices, and continued challenges faced by farmers/fertilizer users in a rising consumption environment have driven continuing consumption for fertilizer use in the region.

Market Trends in India

India is the dominant country in the Asia Pacific fertilizers market primarily because of the large agriculture base for fertilizer use as well as the governments subsidies. Government initiatives such as the "Soil Health Card" and PM-KISAN scheme promote balanced fertilizer use practices to enhance grower's productivity. Continued demand for food grains in India and increasing government and private investments into agribusiness and rural infrastructure's will all be advised on continue and have made for consistent fertilizer consumption in India going forward.

Fertilizers Market Volume and Share, By Region, 2024- 2034 (%)

| By Region | Market Volume Shares (%)2024 | Market Volume (Million Tons)2024 | Market Volume Shares (%)2034 | Market Volume (Million Tons)(2034) | Market CAGR (2025-2034) | ||||

| North America | 20.62 | % | 39.8 | 21.4 | % | 56.2 | 2.76 | % | |

| Europe | 13.35 | % | 25.8 | 14.8 | % | 38.7 | 3.68 | % | |

| Asia Pacific | 52.08 | % | 100.6 | 51.0 | % | 133.8 | 3.02 | % | |

| Latin America | 8.40 | % | 16.2 | 7.7 | % | 20.1 | 2.98 | % | |

| Middle East & Africa | 5.55 | % | 10.7 | 5.1 | % | 13.3 | 3.80 | % | |

Why North America showing up as the Fastest Growing Region in Fertilizers Market ?

North America expects the fastest growth in the market during the forecast period. The growth of the market is attributed due to the increased adoption of precision farming, organic, and specialty fertilizers in the region. Also, there is a growing awareness of soil health in North America and farmers are shifting toward sustainable products, such as slow-release fertilizers and bio-based fertilizers, to increase productivity while minimizing the impact on the environment and their natural resources. Furthermore, the tech-enabled agricultural systems and increased funding towards smart farming in North America is providing growth.

Market Trends in the U.S.

The United States is leading this growth with their established farming infrastructure, the presence of many fertilizer manufacturers in the country, and the widespread utilization of innovative fertilizers in their farming practices. Furthermore, the USA government has allowed for support of climate-smart agriculture that provides further fertilizer adoption.

Competitive Landscape in the Fertilizers Market

- Nutrien Ltd- World's largest fertilizer producer; supplies nitrogen, phosphate, and potash fertilizers.

- Yara- Global leader in sustainable crop nutrition; focuses on nitrogen-based fertilizers and precision farming.

- ICL- Produces potash and phosphate fertilizers; emphasizes specialty fertilizers and innovation.

- The Mosaic Company- Major producer of phosphate and potash fertilizers; vertically integrated operations.

- CF Industries and Holdings, Inc.- Specializes in nitrogen-based fertilizers; has a vast production and distribution network.

- Nufarm- Provides liquid fertilizers and crop protection products, strong in specialty and value-added solutions.

- SQM SA- Produces specialty fertilizers including potassium nitrate, leader in iodine and lithium sectors too.

- OCP Group- World's largest exporter of phosphate rock and derivatives; based in Morocco.

- K+S Aktiengesellschaft- Supplies potash and salt-based fertilizers; strong presence in Europe and the Americas.

- EuroChem Group- Vertically integrated producer of nitrogen, phosphate, and potash fertilizers; global operations.

For more information, visit the Towards Chem and Materials website or email the team at sales@towardschemandmaterials.com| +1 804 441 9344

More Insights in Towards Chem and Materials:

- Cyclohexanone Market: The global cyclohexanone market volume is calculated at 4.97 million tons in 2024, grew to 5.1 million tons in 2025 and is predicted to hit around 6.48 million tons by 2034, expanding at healthy CAGR of 2.70% between 2025 and 2034.

- U.S. Nitrogenous Fertilizers Market : The U.S. nitrogenous fertilizers market volume is calculated at 12,151.6 kilo tons in 2024, grew to 12,459.04 kilo tons in 2025 and is predicted to hit around 15,600.66 kilo tons by 2034, expanding at healthy CAGR of 2.53% between 2025 and 2034.

- Specialty Fertilizers Market : The global specialty fertilizers market volume is calculated at 30.23 million tons in 2024, grew to 31.75 million tons in 2025, and is projected to reach around 49.33 million tons by 2034.The market is expanding at a CAGR of 5.02% between 2025 and 2034.

- Phosphate Fertilizers Market : The global phosphate fertilizers market size was USD 70.11 billion in 2024 and is expected to be worth around USD 124.97 billion by 2034, growing at a compound annual growth rate (CAGR) of 5.95% during the forecast period 2025 to 2034.

- Biopharma Plastic Market : The global biopharma plastic market size is expected to be worth around USD 13.35 billion by 2034 from USD 6.19 billion in 2024, growing at a CAGR of 7.99% during the forecast period 2025 to 2034.

- Synthetic Graphite Market : The global synthetic graphite market size is expected to be worth around USD 16.05 Billion By 2034, from USD 8.91 Billion in 2025, growing at a CAGR of 6.75% during the forecast period from 2025 to 2034.

Fertilizers Market Top Key Companies:

- Nutrien Ltd

- Yara

- ICL

- The Mosaic Company

- CF Industries and Holdings, Inc.

- Nufarm

- SQM SA

- OCP Group

- K+S Aktiengesellschaft

- Eurochem Group

- Sociedad Quimica y Minera de Chile SA

What is Going Around the Globe?

- In December 2024 Major Indian fertilizer company IFFCO announced a new nano NPK fertilizer is in development and is currently in need of government approval. The product is to be produced at IFFCO's Kandla location and will be available shortly via retail.

- In January 2025, Super Crop Safe Ltd., a leading agrochemical and biotechnology company, introduced a new biofertilizer called Super Gold WP+. It is a new postmix with inoculated mycorrhiza and important nutrients to reduce reliance on chemical fertilizers and promote sustainable agriculture.

-

In May 2025, Mosaic Values introduced Neptunion, a new water‐soluble biostimulant in China that increases crop resilience against drought, salinity, and heat by improving stress resistance in fertilizers .

Fertilizers Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2019 to 2034. For this study, Towards Chem and Materials has segmented the global fertilizers Market

By Form

- Solid Fertilizers

- Granules

- Powder

- Liquid Fertilizers

- Solution

- Suspension

- Gaseous Fertilizers

- Ammonia (used in large-scale farming)

By Type

- Chemical Fertilizers

- Biofertilizers

By Crop-Type

- Cereals & Grains

- Frutis & Vegetables

- Oilseeds & Pulses

- Others

By Application

- Fertigation

- Foliar

- Soil

By End User

- Individual Farmers

- Agricultural Cooperatives

- Commercial Growers

- Government & Public Sector

- Research & Educational Institutions

By Distribution Channel

- Direct Sales

- Distributors & Wholesalers

- Retail Stores

- Online/E-commerce Platforms

- Cooperatives

By Regional

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East Africa

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/price/5578

About Us

Towards Chem and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: sales@towardschemandmaterials.com

Web: https://www.towardschemandmaterials.com/

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.